When someone dies, people around you want motion. They want progress. They want closure. That’s human. But the early estate process has a trap: the actions that feel most helpful are often the ones that create the most cleanup later.

We’re going to be direct here, because the stakes are real. Avoiding a handful of common mistakes can save months of frustration, reduce family conflict, and protect the estate’s value.

(This is general information, not legal or tax advice. Rules vary by state and by institution.)

The goal in the early days

In the first week, the win is not “getting everything done.” The win is:

- securing property and information

- preventing waste and fraud

- documenting everything

- avoiding irreversible decisions until authority is clear

With that framing, here are the mistakes we see most often.

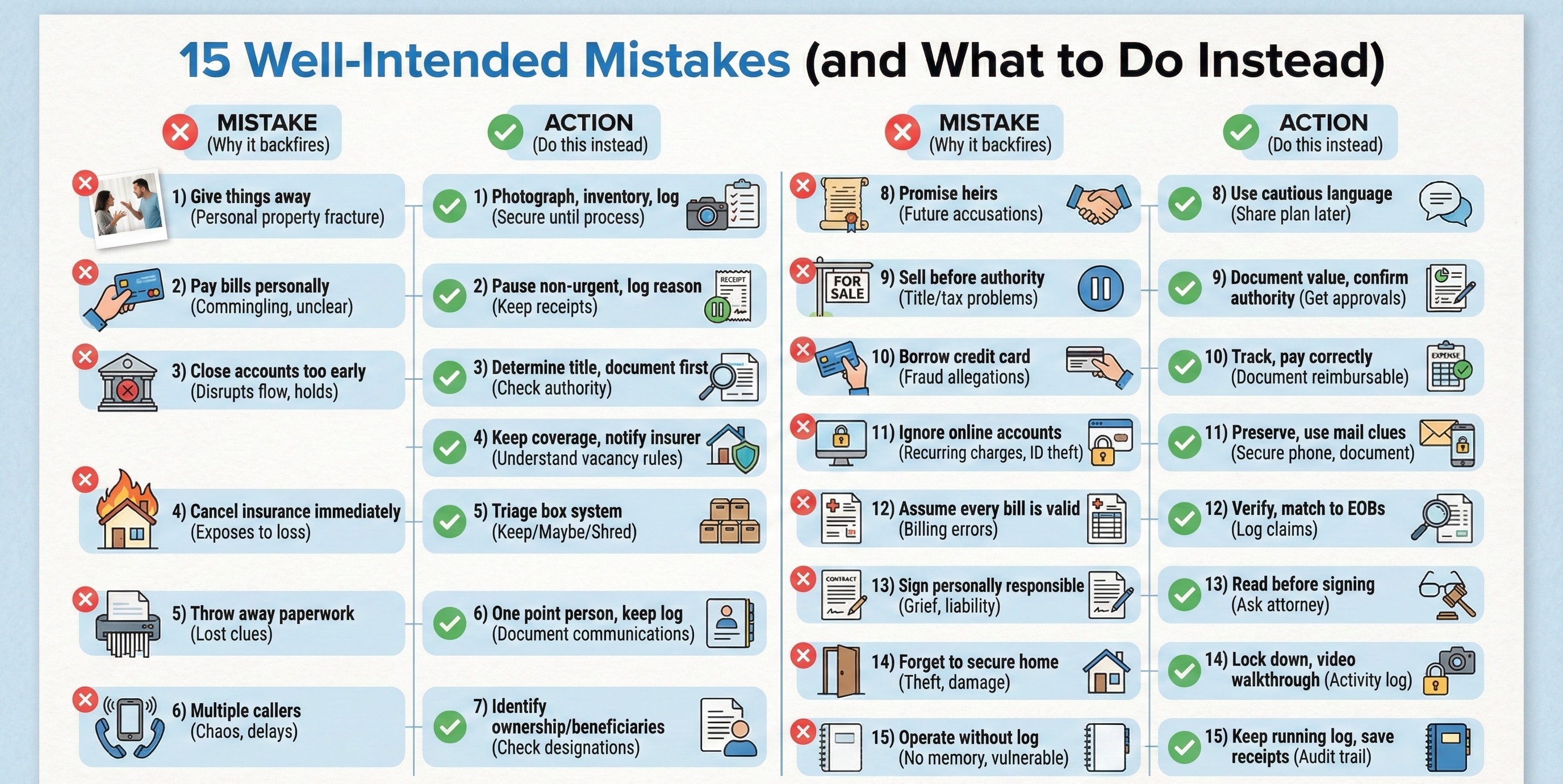

15 well-intended mistakes (and what to do instead)

1) Don’t start “giving things away” because everyone agrees

Why it backfires: Personal property is where families fracture. Even when everyone thinks they agree, memories and emotions change fast—especially once money or heirlooms are involved.

Do this instead: Photograph and inventory items first. If something must be removed for security, log it, label it, and keep it accessible until a fair process is defined.

2) Don’t pay the decedent’s bills from your personal account

Why it backfires: It creates commingling, reimbursement disputes, and unclear accounting. In some situations it can also create the appearance of prioritizing one creditor over another.

Do this instead: Pause non-urgent payments until authority is established. If something truly must be paid to protect value (e.g., preventing property damage), keep receipts and log the reason.

3) Don’t close bank accounts “to simplify things”

Why it backfires: Closing too early can disrupt deposits, refunds, benefit reversals, and tax reporting. It can also trigger holds and make it harder to trace transactions.

Do this instead: First determine how the account is titled (sole, joint, payable-on-death) and what authority the bank requires. Document balances and statements before any changes.

4) Don’t cancel insurance immediately

Why it backfires: Canceling homeowners or auto insurance can expose the estate to loss. Vacant homes and idle vehicles are risk magnets.

Do this instead: Keep essential coverage in place until ownership and plans are clear. If the home is vacant, notify the insurer and ask about vacancy rules so you don’t accidentally void coverage.

5) Don’t throw away paperwork because it “looks like junk”

Why it backfires: The mail and paper piles often contain the clues to missing assets, unknown debts, subscriptions, and benefits.

Do this instead: Create a simple “triage box” system: Keep / Maybe / Shred Later. Anything financial, medical, legal, or insurance-related goes into Keep or Maybe.

6) Don’t let multiple family members call banks, creditors, and institutions

Why it backfires: Conflicting stories get recorded in call notes. Different people receive different instructions. It turns into chaos and delays.

Do this instead: Choose one point person for institutional communications. Keep a call log with date, time, who you spoke with, and what they required.

7) Don’t assume “the will controls everything”

Why it backfires: Many assets transfer outside a will (beneficiary designations, joint accounts, trust-owned assets). Misunderstanding this creates wrong assumptions and bad decisions.

Do this instead: Treat “how it’s owned” as the controlling factor. Identify beneficiary designations and account titles before making any distribution promises.

8) Don’t promise heirs what they’ll receive (or when)

Why it backfires: Early promises become future accusations. And you may not yet know debts, taxes, or even the full asset picture.

Do this instead: Use language like: “We’re inventorying everything and will share a clear plan once we know what exists, what transfers automatically, and what debts/taxes apply.”

9) Don’t sell property or vehicles before authority and documentation are clear

Why it backfires: You can create title problems, tax problems, or fairness issues if values weren’t documented. You can also create legal exposure if you act without authority.

Do this instead: Document value first (photos, statements, and a defensible valuation approach). Confirm who has legal authority to sell and what approvals are required.

10) Don’t let anyone “borrow” the deceased’s credit card “just to cover expenses”

Why it backfires: That’s a fast path to fraud allegations, bank disputes, and family conflict—even if the intent was good.

Do this instead: Track funeral and estate expenses explicitly and pay them through the correct channel once authority is in place. If immediate expenses must be covered, document them as reimbursable with receipts.

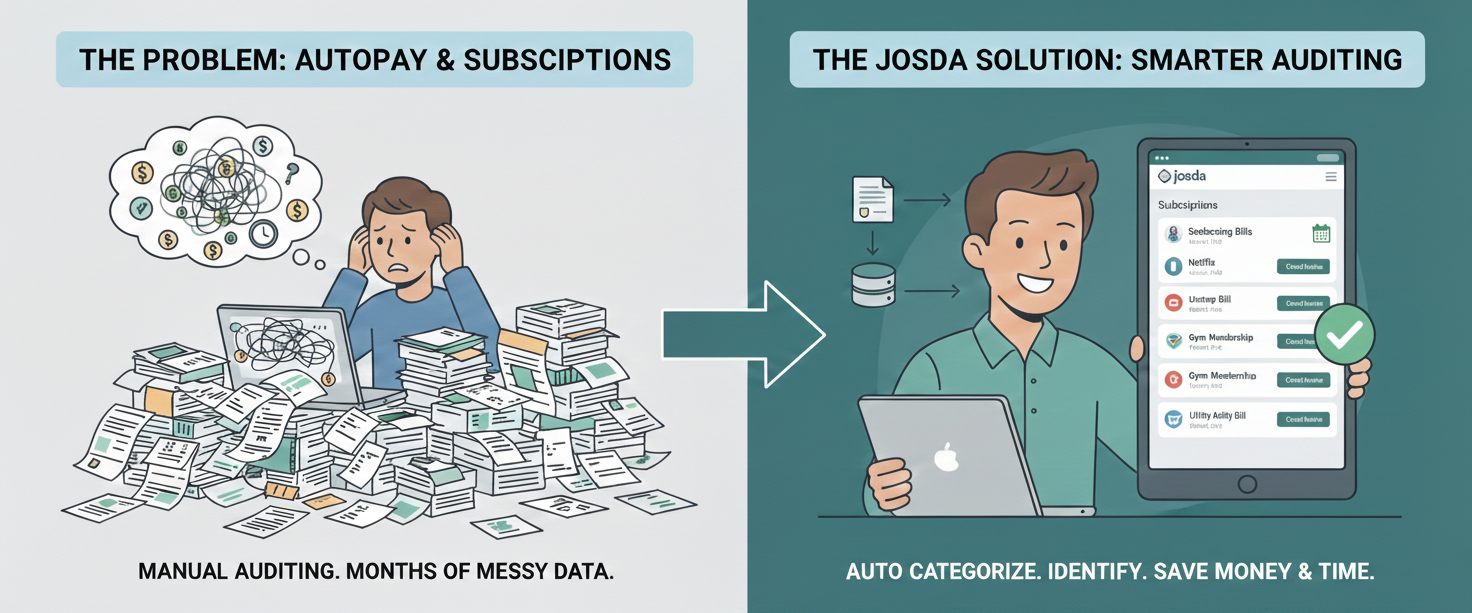

11) Don’t ignore online accounts and phone access until “later”

Why it backfires: Two problems show up: (1) recurring charges continue quietly, and (2) identity theft risk increases after a death.

Do this instead: Preserve what you can responsibly. Use the mail and statements to identify subscriptions. Secure the phone if possible and document access steps. Avoid guessing passwords or doing anything that could be interpreted as unauthorized access.

12) Don’t assume every bill is valid (especially medical bills)

Why it backfires: Billing errors are common, and some bills get sent to family members in ways that make them feel personally responsible when they may not be.

Do this instead: Verify. Match medical bills to EOBs/insurance records when available. Log claims. Don’t pay fast just to reduce stress—verify first.

13) Don’t sign anything as “personally responsible”

Why it backfires: Grief makes people agree to language they would never accept otherwise. Sometimes vendor forms, facility agreements, or creditor paperwork includes personal liability language.

Do this instead: Read before signing. If a document implies personal responsibility, pause. When in doubt, ask a qualified attorney before you put your name on it.

14) Don’t forget to secure the home and document what’s inside

Why it backfires: Theft, damage, and disputes over missing items become “your fault” by default if you’re the coordinator.

Do this instead: Lock it down, take a walkthrough video, and keep an activity log. If others need access, set rules and document who entered and why.

15) Don’t operate without an activity log and receipts

Why it backfires: Without documentation, you will not remember why decisions were made, and you’ll be vulnerable to “you did that wrong” conversations later.

Do this instead: Keep a running log of actions, calls, expenses, and decisions. Save receipts in one place. Treat it like a lightweight audit trail.

If you already did one of these, you’re not doomed

Most families make at least one of these mistakes. The fix is usually “document, slow down, and unwind cleanly.”

Here’s the recovery plan:

- Stop further action in the problem area (no more distributions, no more random payments).

- Document what happened: dates, amounts, who was involved, what was moved/sold.

- Preserve evidence: photos, statements, receipts, messages.

- Get the authority question answered (executor/administrator/trustee).

- Create a clean ledger: what left the estate, why, and whether reimbursement is needed.

.svg)

.svg)

.svg)

.svg)