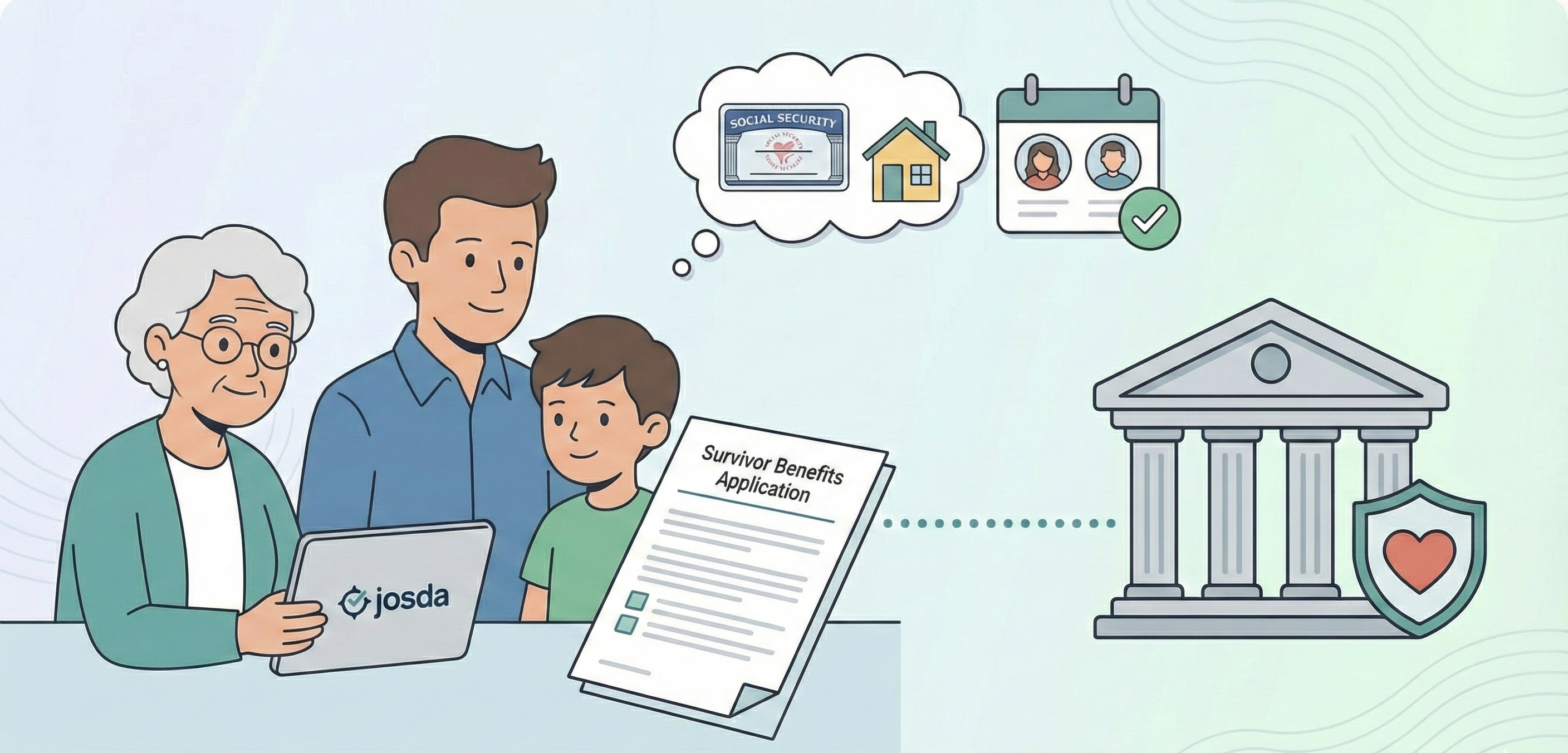

When someone dies, Social Security may be able to replace part of their income for the people who depended on them. The challenge is that “survivor benefits” is an umbrella term: different family members can qualify under different rules, and the application process is not fully online. This guide will help you quickly figure out (1) whether you might qualify and (2) what to do next.

(This is general educational information, not legal or tax advice.)

What are Social Security survivor benefits?

Survivor benefits are monthly payments to certain family members of a person who worked and paid Social Security taxes. There is also a one-time lump-sum death payment in some cases.

Who might qualify?

Survivor benefits generally fall into four buckets: spouse (or ex-spouse), children, and dependent parents.

1) Surviving spouse (widow or widower)

You may qualify if you were married to the person who died and you are:

- Age 60+ (reduced benefits can start as early as 60), or

- Age 50+ and disabled, or

- Any age if you are caring for the deceased person’s child who is under 16 or disabled, and that child is receiving Social Security benefits.

If you remarry: you usually can’t receive surviving spouse benefits if you remarry before age 60 (or before 50 if disabled). Remarrying after those ages generally does not block survivor benefits based on the prior spouse’s record.

2) Surviving divorced spouse

You may qualify on an ex-spouse’s record if:

- You are age 60+ (or 50–59 and disabled), and

- The marriage lasted at least 10 years.

Exception: the age and 10-year rules may not apply if you are caring for the deceased worker’s eligible child (under 16 or disabled) who is entitled on the worker’s record.

3) Children (and sometimes stepchildren/grandchildren)

A child may qualify if they are:

- Unmarried and under 18, or

- 18–19 and in K–12 school full time, or

- Any age if they had a disability that began before age 22.

In certain circumstances, Social Security can also pay benefits to stepchildren, grandchildren, step-grandchildren, or adopted children.

4) Dependent parents

A parent may qualify if they are:

- Age 62+, and

- Were receiving at least half of their support from the deceased worker.

What can survivor benefits pay?

The amount depends on the deceased person’s earnings record and the survivor’s relationship/age. In typical cases:

- A surviving spouse at full retirement age (for survivors) can receive about 100% of the worker’s basic benefit amount.

- A surviving spouse age 60 to full retirement age typically receives 71% to 99% (reduced for starting earlier).

- A surviving spouse caring for a child under 16 can receive 75%.

- A child typically receives 75%.

Family maximum: There’s a cap on how much can be paid to a family each month on one worker’s record—often 150% to 180% of the worker’s benefit amount. If multiple people qualify, each person’s payment may be reduced to stay under the cap.

Working while receiving benefits: If you’re under full retirement age for survivors and you work, benefits may be reduced if earnings exceed annual limits (those limits change over time).

The $255 one-time lump-sum death payment

Social Security may pay a one-time $255 death payment to a qualifying spouse. If there is no eligible spouse, certain children may qualify (including minors, certain students 18–19, or a child disabled before a specified age). You generally must apply within 2 years of the death.

How to start: the practical checklist

Step 1: Report the death (and don’t assume it’s already handled)

Often, a funeral home reports a death, but you should still make sure Social Security has been notified. The SSA’s general guidance is to call 1-800-772-1213 (TTY 1-800-325-0778) during business hours.

Step 2: Apply promptly (delays can cost money)

You generally cannot apply for monthly survivors benefits online. SSA advises applying by phone or at a Social Security office. Also, SSA notes that for some claims, benefits are paid from when you apply—not from the date of death—so delaying can reduce what you receive.

Step 3: Gather the documents SSA will ask for

SSA commonly requests items like:

- Proof of death (death certificate or a statement from the funeral home)

- Your Social Security number and the deceased person’s Social Security number

- Your birth certificate

- Marriage certificate (if applying as spouse)

- Divorce decree (if applying as surviving divorced spouse)

- Children’s birth certificates and Social Security numbers (if applying for children)

- The worker’s W-2s or self-employment tax return for the most recent year

- Bank account/routing info for direct deposit

Important: SSA explicitly says do not delay filing just because you’re missing documents—they can help you obtain them.

Step 4: Call to apply or set an appointment

You can apply by calling SSA’s national number or visiting a local office; scheduling ahead can reduce time spent waiting.

Two common “survivor benefit” situations people miss

- Divorced survivors: If you were married 10+ years, you may be eligible even if your ex-spouse remarried—many people never check.

- Children and caregiving spouses: A surviving spouse of any age may qualify if they’re caring for an eligible child (under 16 or disabled). That can matter even if the spouse is decades away from age 60.

.svg)

.svg)

.svg)

.svg)